Dear Chair Tridico and Distinguished Members of the FISC Subcommittee and National Parliaments,

Thank you for the opportunity to discuss the taxation of digital activities in the EU. I am Cristina Enache, Economist at Tax Foundation Europe.

Today, I will cover three aspects of digital services taxes (DSTs). I will begin by analyzing the design of DSTs and their economic incidence—who ultimately bears the cost rather than who remits the tax. Next, I will examine the international responses and trade-related consequences that countries may face when enforcing a DST. Finally, I will assess the revenue generated by DSTs and explore alternative tax instruments, such as value-added taxes (VATs), that offer more effective and pro-growth tax solutions.

The Problem with Digital Services Taxes

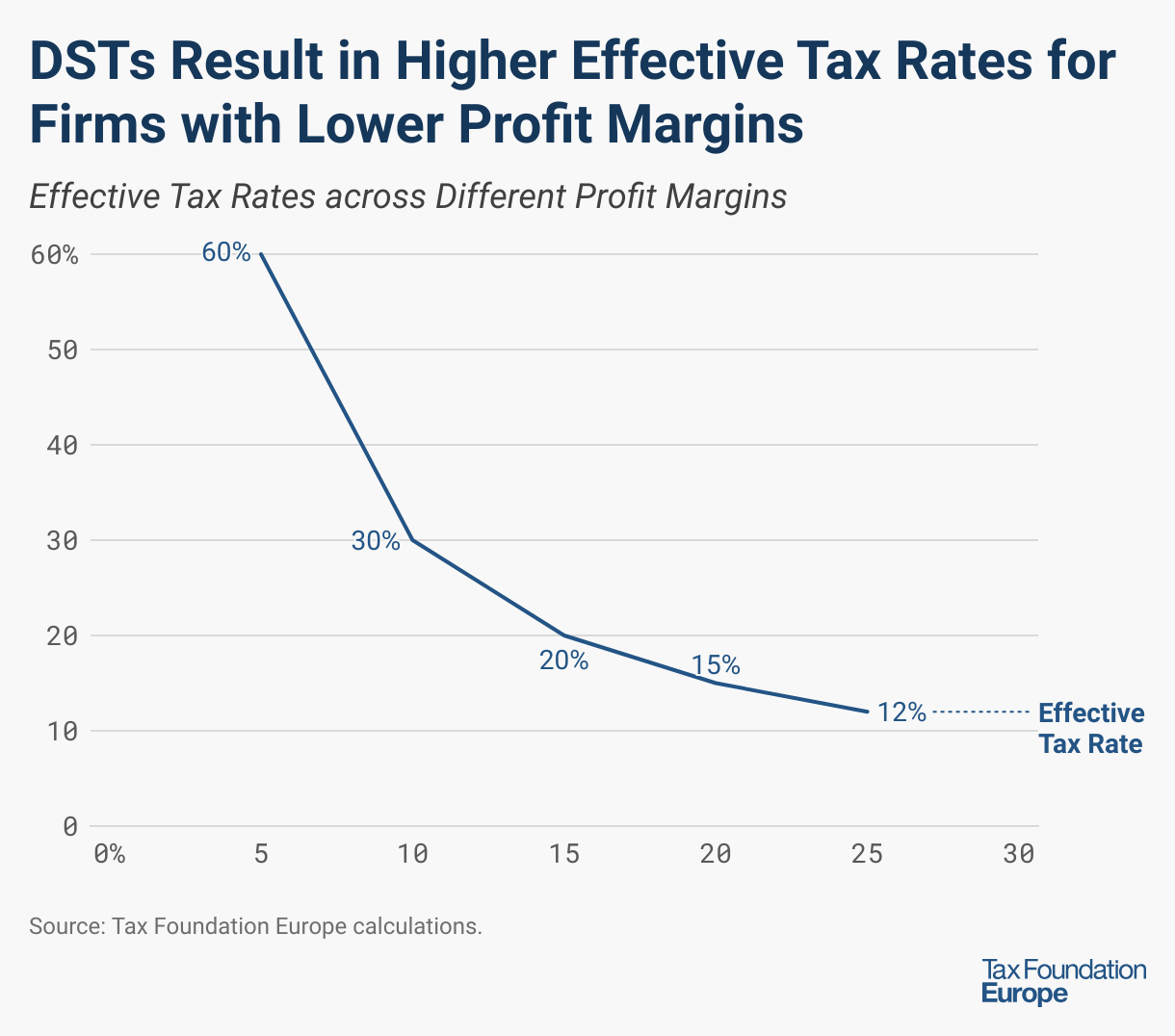

Unlike corporate income taxes, DSTs are levied on revenues rather than profits. This ignores profitability. Historically, Europe has turned away from turnover taxes because seemingly low tax rates can translate into high effective tax burdens. For example, if a company has €100 in revenue and €85 in costs, it will earn €15 in profit. If a 3 percent DST is applied to that revenue, the company would owe €3 in tax (3 percent of €100 in revenue). For this company, a 3 percent tax on revenue equals a 20 percent tax on profits (3 percent of €15). The nearby figure shows how different profit margins for that same company earning €100 in revenue relate to different effective tax rates. If that company only earned a 5 percent profit margin, the effective tax rate with a 3 percent DST would be 60 percent. With a 25 percent profit margin, the effective tax rate falls to 12 percent.

As you can see, this leads to a disproportionate tax burden being placed on companies with lower profit margins—the less profitable a company is, the higher its effective tax rate becomes. This is regressive.

In addition, DSTs are discriminatory in terms of company size. The revenue thresholds result in the tax only being applied to large multinationals. While this can ease the overall administrative burden, it also provides a relative advantage for businesses below the threshold and creates an incentive for businesses operating near the threshold to alter their behavior. Because these thresholds aren’t adjusted for inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spendin, more firms will likely fall within their scope over time. Likewise, digital businesses are at a relative disadvantage to non-digital businesses operating in a similar field.

Additionally, a recent research paper by economists Dominika Langenmayr and Rohit Reddy Muddasani shows that the attempt to target big digital platforms misses the mark as the cost mostly falls on European consumers.

Retaliatory Measures

DSTs, which function like tariffs on certain services, are designed to be discriminatory; they target specific industries dominated by US companies. The US government has voiced opposition to DSTs over the last decade, with President Trump using Section 301 investigations in his first term, and, more recently, the US Congress threatening the Section 899 retaliatory tax. While section 899 was removed from the One Big Beautiful Bill Act, the issue of DSTs remains contentious. Until a true consensus is found on how to handle the taxation of the digital economy, escalating retaliatory measures will harm all parties involved.

Revenue Impact and Policy Alternatives

Regardless, many European governments are seeking to increase revenue. DST revenue in Austria, France, Italy, Spain, Turkey, and the UK ranged from €103 million (Austria) to €1.03 billion (the UK) in the most recent year revenue was reported. Austria’s DST is much narrower than the others in the sample because it applies only to digital advertising. In all cases, the amounts raised are less than one percent of the country’s general revenue. Turkey’s DST brings in the most at 0.14 percent of total revenues.

Recent Revenue Raised from Selected Digital Services Taxes

| Country | Most Recent Year for Official DST Revenue Reported | DST Revenue (local currency) in Millions | DST Revenue (in EUR) in Millions |

|---|---|---|---|

| Austria | 2023 | € 103 | |

| France | 2024 | € 756 | |

| Italy | 2024 | € 455 | |

| Spain | 2024 | € 375 | |

| Turkey | 2024 | ₺ 15,561 | € 322 |

| United Kingdom | 2025 | £900 | € 1,032 |

Note: These countries have been selected because they report digital services tax revenue separately as a line item.

Source: Tax Foundation Europe analysis of national budget documents and announcements.

If European policymakers are worried about raising more money from digital services, then they should continue reforming their VATs to effectively tax these services at the point of consumption. Additionally, broadening the VAT tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. by eliminating reduced rates and exemptions would substantially increase the VAT revenue while causing fewer distortions in the economy. Finally, the VAT is trade-neutral and does not discriminate between firms.

Since DSTs deliver limited revenue, shift the burden to European consumers, and risk provoking trade disputes, it’s time for policymakers to rethink their approach. Policymakers should be honest about what tax policy can and cannot do. The primary goal of tax policy is to raise revenue, and there are certainly more efficient ways to do so than DSTs.

Note: Tax Foundation Europe is a nonpartisan think tank focused on improving tax policies across Europe to foster economic growth and opportunity. Tax Foundation Europe is a nonprofit international association under Belgian law (AISBL), governed by its statutes (dated 20 February 2024).

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe