The brief’s key findings are:

- The new “no tax on overtime” law – in effect through 2028 – could encourage workers to change their behavior.

- The changes could involve: 1) seeking more overtime hours; or 2) collaborating with employers to reclassify some work as “overtime.”

- Policymakers should keep an eye on the issue due to potential revenue loss since:

- while the current share of hourly workers with overtime pay is modest, many are close to exceeding the 40-hour threshold; and

- more workers still – both hourly and salaried – could benefit from accepting lower base pay and redefining some of their work as “overtime.”

Introduction

Economics 101 teaches that it is a bad idea to design taxes that distort behavior. Yet the “No Tax on Overtime” provision in the One Big Beautiful Bill Act (OBBBA) – which is in effect from January 1, 2025 to December 31, 2028 – could cause behavior to change in two ways. First, workers who now enjoy a higher after-tax wage could seek more overtime hours. Second, employees and employers could collaborate to reclassify some regular work as “overtime.”

To provide a baseline for possible changes in overtime pay, this brief describes the share of workers who regularly receive overtime and how that varies by age; how many might be able to receive overtime simply by working a bit longer; and the share of workers who could benefit from their employers re-classifying their pay to achieve tax-preferred overtime.

The discussion proceeds as follows. The first section describes overtime work in the United States and the OBBBA overtime provision. The second section describes the data from the American Time Use Survey that underlies the analysis. The third section provides the results, which show that while the share of workers who receive overtime now is relatively small, many workers have hours near the threshold, and more still could benefit from a change in their compensation structure. The fourth section concludes that, during the next three years, researchers and policymakers should monitor how the share of earnings from overtime evolves and why.

Background

This section first lays out the federal overtime rules, then describes how the OBBBA changes the tax treatment of overtime, and finally discusses how the changes could affect overtime pay.

Overtime Pay and the OBBBA

The Fair Labor Standards Act (FLSA) governs overtime pay for both hourly and salaried workers.1 The legislation mandates that hourly employees should be paid at least 1.5 times their usual rate for each hour worked over 40 during a week.2 For salaried workers, the FLSA only mandates overtime pay for those making $35,568 or less.3 For salaried workers earning above that threshold, overtime pay is still required unless their employment falls within an exemption, such as executive and professional workers.4

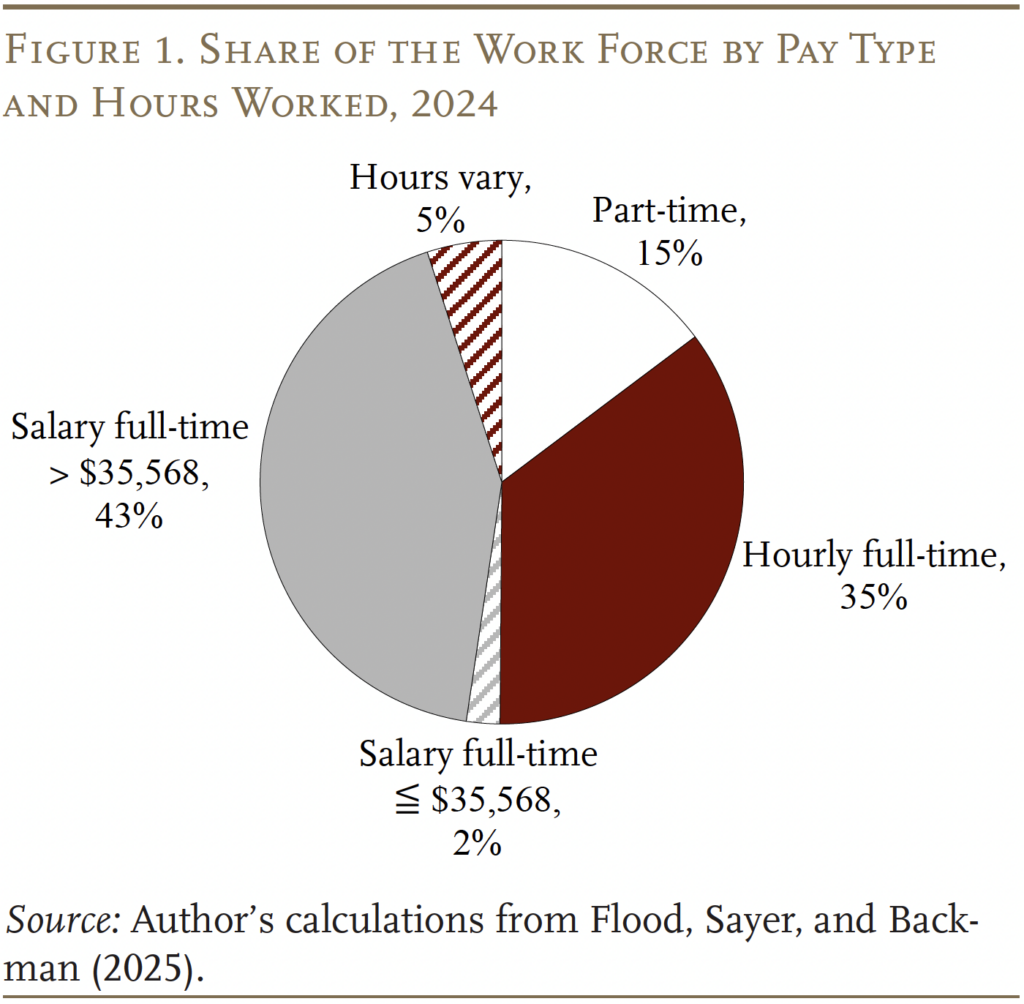

Figure 1 shows that, in 2024, over a third of workers could be eligible to receive overtime under the FLSA in that they were working full-time and: 1) being paid hourly (35 percent); or 2) were salaried and making less than $35,568 (2 percent). Another 43 percent were salaried and making over $35,568, so their employers were likely to declare them exempt. The remaining 20 percent were either working part-time or variable hours.

OBBBA Changes

How does the OBBBA potentially change the picture? Prior to the OBBBA, overtime pay was taxed as ordinary income; now, a maximum of $12,500 of overtime pay can be deducted from taxable income. This maximum deduction is reduced by $100 for each $1,000 earned over $150,000, so the $12,500 is phased out completely by $275,000.5 Note that the deduction applies only to the 50-percent overtime bonus specified by the FLSA, not to the base pay. That is, if a worker earns $20 regularly and $30 when working overtime, only the additional $10 is deductible.

Potential Distortions under OBBBA

The favorable tax provisions under OBBBA could affect overtime in two ways. On one side, workers who already receive or are close to receiving tax-deductible overtime pay could ask to work more hours. This increase in employment would generate new hours worked and more tax revenues. Alternatively, hourly employees and their employers could collaborate by reducing base pay and exaggerating overtime, which could cost the government money without generating any new hours worked. For example, a worker earning $25 an hour for 40 hours a week could reduce their compensation to a state’s minimum wage of, say, $15 and have their employer record 17.8 hours of overtime worked to produce the same compensation without any change in hours worked.6

For salaried workers, employers could simply stop asking for an exemption for workers who already work enough hours to claim overtime. The employer could then reduce the worker’s base pay to keep the worker’s pay steady, which again would put the worker ahead in view of the favorable taxation of overtime pay. Such a response could run afoul of the FLSA because it would suggest that the worker may have been inappropriately exempted before the OBBBA; still, the temptation exists.7 And, unlike with the adjustment imagined for hourly workers, this reclassification requires no misreporting of hours.8

So how many workers might add hours and gain access to tax-deductible pay? And how many workers and employers might collaborate to increase the share of wages paid as overtime pay? The answer is unclear – the main research on the topic is decades old.9 The next section turns to the data to take a preliminary look at these issues.

Data

This brief uses the American Time Use Survey (ATUS) to examine the current receipt and potential receipt of overtime pay by age. For hourly workers, the ATUS asks a direct question about usual overtime pay received each week. The survey does not ask this direct question for salaried workers, since few qualify for overtime. As a result, it is necessary to combine a second ATUS question, which lumps together information on overtime, tips, and commissions, with overtime-related questions from the Current Population Survey.10

With these estimates in hand, the analysis will turn to the question of how many workers might be able to start claiming overtime hours either by: 1) working more hours; or 2) collaborating with their employer to reclassify hours as overtime. The first quantity is relatively simple to estimate. For hourly workers, the brief defines it as the share of workers who usually work 35 or more hours a week – and thus could easily work just a bit more and exceed the FLSA’s 40-hour threshold – but report that they do not usually receive overtime. For salaried workers, the calculation is the same, but adds the restriction that income falls below the $35,568 threshold.

The second quantity – the share of workers who could benefit from taking lower regular pay and claiming more pay as overtime – is more complicated. For hourly workers, this share is estimated by first calculating the amount an individual would make in 40 hours at their state’s minimum wage. If that amount falls below their usual weekly earnings, then the second step is to determine how many hours of overtime they would need to make themselves whole.

For salaried workers, the question is the portion of salary that could be made tax deductible for those who: 1) claim not to regularly receive overtime (i.e., must be exempt); 2) claim to usually exceed 40 hours a week and thus must currently be declared as exempt; and 3) earn less than the OBBBA’s $275,000 ceiling. If these workers were reclassified as non-exempt, they could simply work the same number of hours and receive tax-deductible overtime in exchange for lower base pay, without cost to their employer.

Results

This section reports the share of workers who received, or are near receiving, overtime pay and then examines what share of workers could benefit from classifying more of their pay as overtime.

Share Receiving Overtime

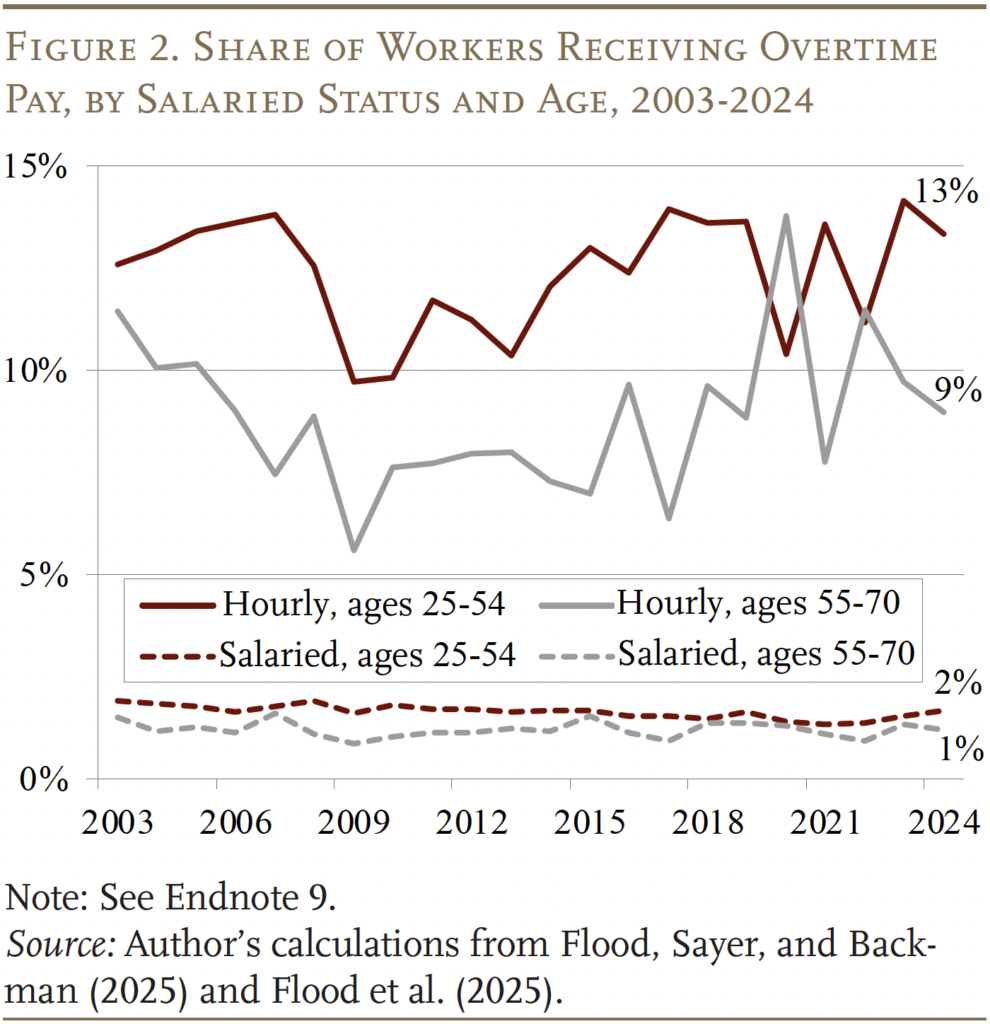

Figure 2 shows the share of hourly and salaried workers who were estimated to have received overtime from 2003 to 2024 for two age groups: those 25-54 and those 55-70. As it turns out, overtime pay is uncommon even among hourly workers, with rates falling below 15 percent for the entire period, and extremely rare for salaried workers.

OK, so overtime pay is not that common. But could the OBBBA encourage workers on the margin to increase their hours?

Share on Margin of Receiving Overtime

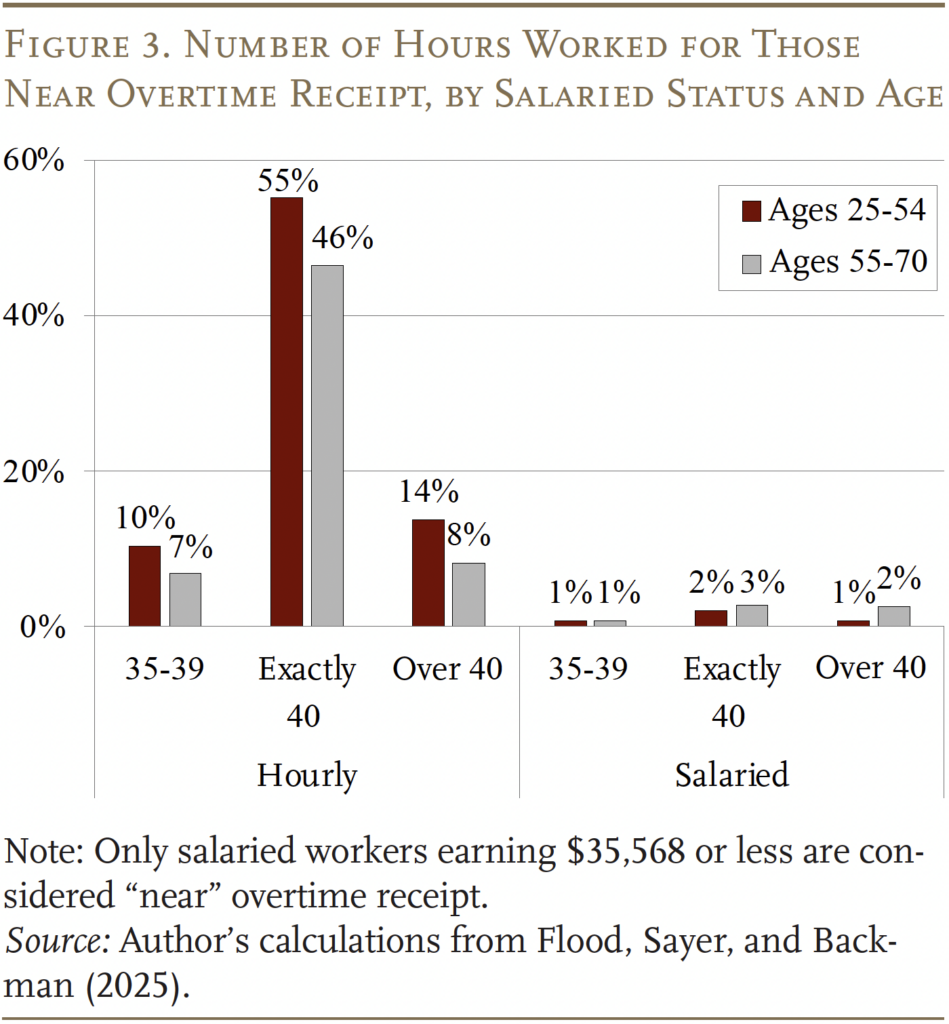

For this exercise, the goal is to estimate the share of hourly and salaried workers in 2024 who meet three criteria: 1) they claim not to regularly receive overtime pay; 2) they usually work hours near where they could begin receiving it; and 3) if salaried, they make below the $35,568 threshold. The results show that most hourly workers who do not receive overtime could work just a bit more to become eligible (see Figure 3). This finding holds for both younger and older workers, although it is slightly larger for younger ones.11

The combination of Figures 2 and 3 can be viewed in two ways. On the one the hand, the large percentage of hourly workers who are eligible or close to being eligible for overtime suggests the OBBBA could cause a big change in work. On the other hand, the fact that few workers – while eligible or close to being eligible – receive overtime pay suggests that employers are not prone to grant more expensive overtime hours.

But what could happen if employers collaborated with employees to grant them “overtime” hours?

Manipulation of Pay Classification

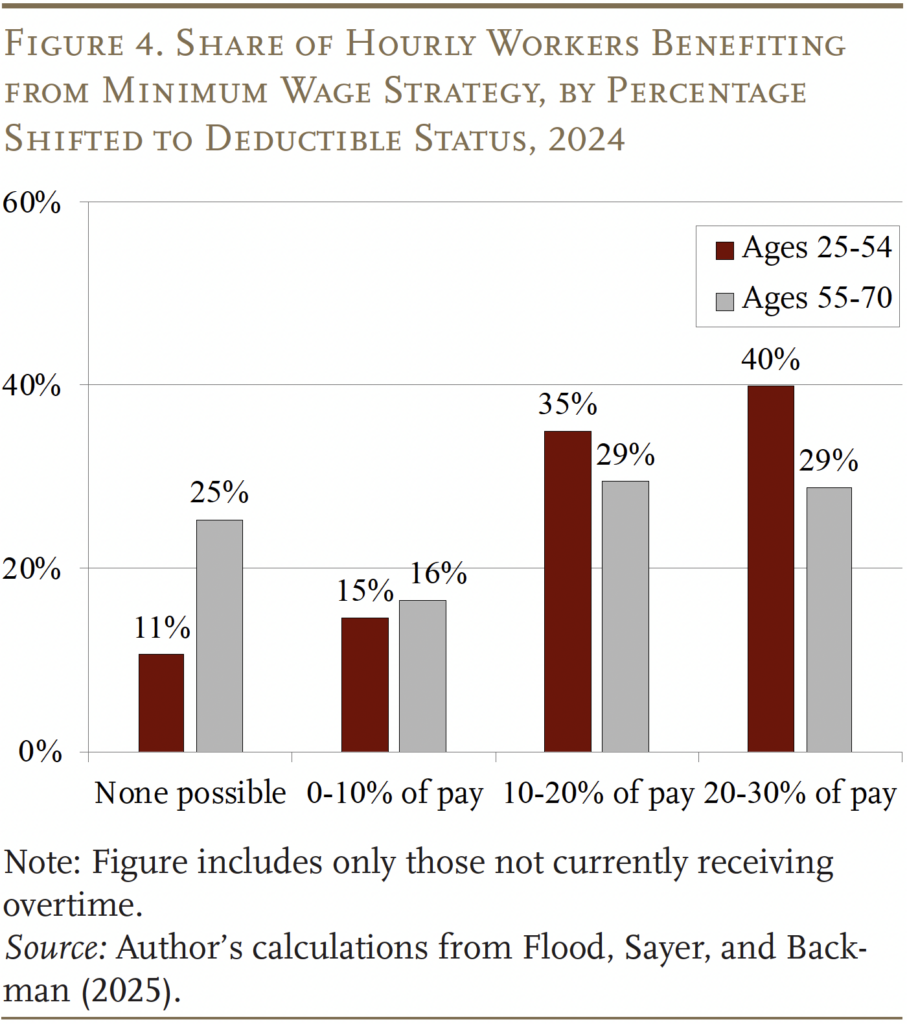

The exercise here is to determine the share of workers that could shift some of their pay from taxable to tax-deductible status. For hourly workers, the exercise assumes bringing the worker’s hourly rate to the minimum wage and setting hours so as to make the worker whole. Figure 4 shows that most hourly workers could benefit from such a reclassification, since, as shown above, they were either at the 40-hour threshold or remarkably close to it. Just 11 percent of younger workers and 25 percent of older workers would be unable to gain some tax advantage from this strategy, and many could shift as much as 20-30 percent of their income to tax-deductible overtime.

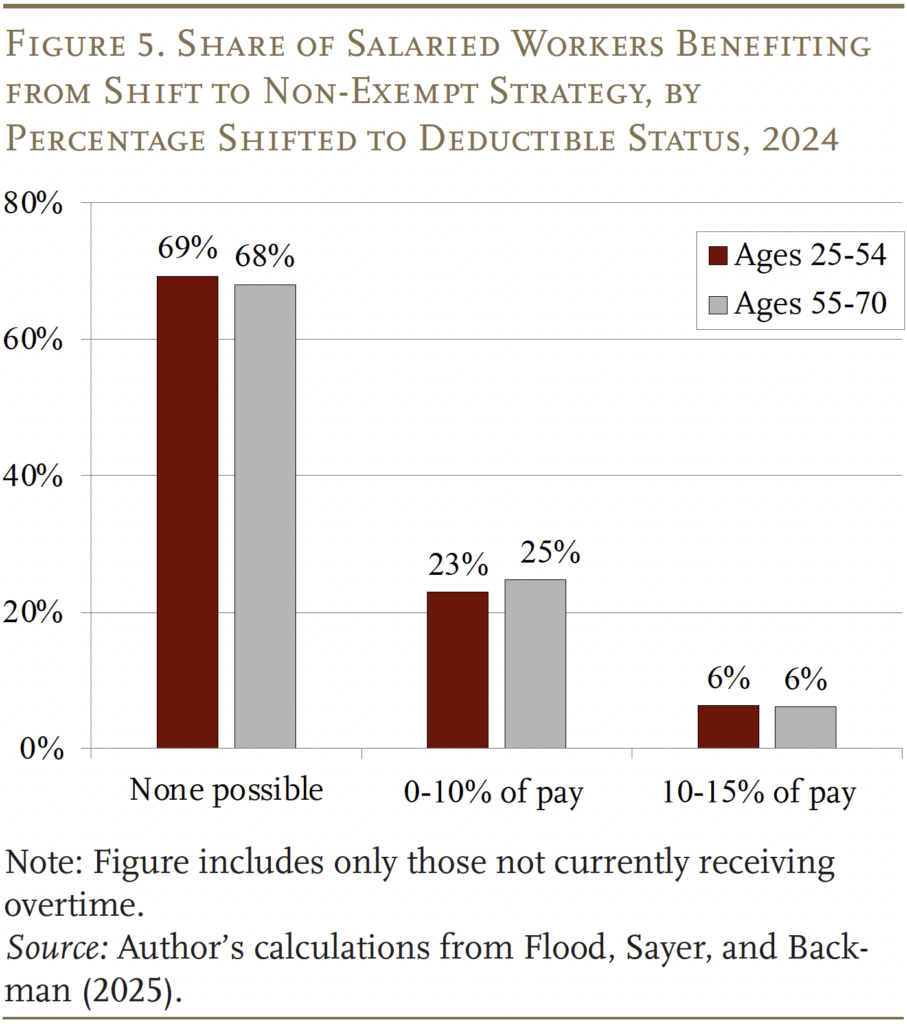

For salaried workers, less overt manipulation could result in tax savings. Employers could simply cease declaring their salaried workers as exempt. As shown in Figure 5, the share of salaried workers affected is lower than for the hourly worker strategy. The main reason is that most salaried workers work 40 hours a week or less (the modal amount is exactly 40 hours), and even when those workers go over 40 hours, it is often not by much.12

In the end, the analyses summarized in Figures 2 through 5 suggest that nearly 60 percent of all workers either: 1) receive overtime now; 2) could work a few more hours and qualify for overtime; or 3) could use one of the two strategies outlined to claim “overtime.” Clearly, the potential impact of OBBBA on behavior is worth keeping an eye on going forward.

Conclusion

Treating some forms of income differently than others can invite changes in behavior to evade taxes. In this case, the OBBBA’s “no tax on overtime provision” could encourage workers to seek more overtime. In fact, the evidence shows that many hourly workers are close to the 40-hour per-week threshold.

The potentially bigger issue is the potential for the manipulation of hours or exemption status to shift some income to tax-deductible overtime pay. While such actions would run afoul of the FLSA, the OBBBA introduces a temptation that was not there before.

Over the remaining three years when this deduction is in effect, it will be important for the Department of Labor to keep track of how many workers are receiving overtime and identify any marked shifts. After all, the analysis suggests that the behavior of many workers could potentially be shifted. These shifts could take the form of more hours worked or, for salaried workers, the simple removal of exempt status. While the currently temporary nature of this new tax deduction may make any large-scale changes unlikely, a failure to keep an eye on the issue could cost the government a considerable amount of money.

References

Carr, Darrell E. 1986. “Overtime Work: An Expanded View.” Monthly Labor Review 109: 36-39.

Flood, Sarah M., Liana C. Sayer, and Daniel Backman. 2025. American Time Use Survey Data Extract Builder: Version 3.3 [dataset]. College Park, MD: University of Maryland and Minneapolis, MN: IPUMS.

Flood, Sarah M., Miriam King, Renae Rodgers, Steven Ruggles, J. Robert Warren, Daniel Backman, Etienne Breton, Grace Cooper, Julia A. Rivera Drew, Stephanie Richards, David Van Riper, and Kari C.W. Williams. 2025. IPUMS CPS: Version 13.0 [dataset]. Minneapolis, MN: IPUMS.

Levine, David. I. and David Lewin. 2006. “The New ‘Managerial Misclassification’ Challenge to Old Wage and Hour Law; or What Is Managerial Work?” Contemporary Issues in Employment Relations: 189-222.

Lyness, Karen S., Janet C. Gornick, Pamela Stone, and Angela R. Grotto. 2012. “It’s All About Control: Worker Control Over Schedule and Hours in Cross-national Context.” American Sociological Review 77(6): 1023-1049.

U.S. Department of Labor. 2026. “Recordkeeping and Reporting.” Washington, DC.